Short Term Rental Tax Kenya: Complete 2026 Guide for Hosts

By Oscar Murimi · Short-Term Rental Specialist, Trubay Stayz

Updated: March 2026⏱ 10 min read⚖️

Reviewed against KRA guidelines, 2026

📌 Quick Answer

Short-term rental tax in Kenya is governed by the Kenya Revenue Authority’s Monthly Rental Income (MRI) Tax — a flat rate of 10% on gross rental income. This applies to landlords and hosts earning between KES 144,001 and KES 10,000,000 per year. Returns are filed monthly through KRA’s iTax portal, with payments due by the 20th of the following month. Hosts earning below KES 144,000 per year (KES 12,000 per month) are currently exempt.

📌 Looking for a short-stay apartment in Nairobi? This guide covers tax obligations for Kenyan hosts. If you are a guest looking for verified furnished apartments to book in Nairobi — from KES 2,800 per night across Westlands, Kilimani, Gigiri, and more — our complete short stay apartments guide has everything you need.

Table of Contents

- Why most Kenyan hosts are unknowingly non-compliant

- How short term rental tax in Kenya works under KRA

- Calculating exactly what you owe — with worked examples

- Filing your short term rental tax return: step by step

- VAT, Digital Service Tax, and other obligations

- Penalties for non-compliance — and how to avoid them

- What changes if you host through a registered company

- Frequently asked questions

Understanding short term rental tax in Kenya is, frankly, one of the topics most Kenyan hosts avoid the longest. It feels complicated, and the consequences of getting it wrong feel distant — until they don’t. The Kenya Revenue Authority has been consistently expanding its monitoring of rental income, and in 2026, digital platforms operating in Kenya are increasingly required to share transaction data with KRA. If you are earning income from hosting guests, the question is no longer whether to comply — it is how to do so correctly, from today, without disrupting the income your property is already generating.

This guide breaks down the full picture of Kenya’s short-term rental tax in plain language. It covers the Monthly Rental Income tax rate, how to file, VAT obligations, Digital Service Tax, penalties, and what changes if you operate through a company. The goal is not just to inform you — it is to leave you with a clear action plan that eliminates uncertainty entirely.

Why Most Kenyan Hosts Are Unknowingly Non-Compliant

The vast majority of Kenyan short-term rental hosts are not evading tax through any deliberate decision. They are simply hosting, receiving payment via M-Pesa or bank transfer, and not connecting that activity to a formal tax obligation. This is a gap that the KRA has been actively closing since 2020, and it is a gap that exposes hosts to penalties, back taxes, and in extreme cases, criminal liability.

The confusion is understandable. Kenya’s Monthly Rental Income tax regime was introduced relatively recently, and its application to short-stay platforms rather than traditional long-term landlords is not widely communicated. Many hosts assume that because they are operating informally — listing on Airbnb, accepting M-Pesa, managing their own property — they fall outside the tax net. They do not.

⚠️ Important

If you have been earning short-term rental income for more than 12 months without filing monthly returns with KRA, you are technically in arrears. The good news is that KRA periodically offers voluntary disclosure programmes that allow hosts to regularise their position without the full weight of penalties. Acting proactively now is far better than waiting for KRA to act first.

How Short Term Rental Tax in Kenya Works Under KRA

The short term rental tax rate in Kenya under the Monthly Rental Income regime is a flat 10% applied to your gross rental income — meaning the total amount your guests pay you before any deductions for expenses, maintenance, or platform fees. This is an important distinction. Unlike personal income tax, the MRI tax does not allow you to deduct mortgage interest, repairs, property management costs, or any other expense. The 10% applies to your total receipts.

| Annual Rental Income | Tax Regime | Rate | Deductions Allowed? | Notes |

|---|---|---|---|---|

| Below KES 144,000/yr (KES 12,000/mo) | Exempt | 0% | N/A | No filing required |

| KES 144,001 – KES 10M/yr (most hosts) | Monthly Rental Income (MRI) | 10% flat | No | Applied to gross income. Monthly returns on iTax. |

| Above KES 10M/yr (high earners) | Personal Income Tax (IT1) | Graduated 10–30% | Yes | Standard tax return. Expenses deductible. |

For most Kenyan short-term rental hosts — particularly those with one or two properties in Nairobi, Mombasa, or Naivasha — the MRI regime applies. A host earning KES 70,000 per month from a Westlands studio owes KES 7,000 in rental income tax each month. A host earning KES 120,000 per month from two Kilimani listings owes KES 12,000 per month. These are not large amounts relative to the income generated, but they are legal obligations, and ignoring them compounds over time.

Already hosting, but not sure where your tax position stands? Our Trubay Stayz host support team can point you to the right KRA resources for your situation. Talk to Our Team →

Calculating Exactly What You Owe — Worked Examples

Abstract percentages are easy to understand. Real numbers are easier to act on. Here are three realistic scenarios for Kenyan short-stay hosts in 2026, showing exactly what each host owes monthly and annually under the MRI regime.

Example 1: Studio Apartment, Roysambu

Monthly bookings total: KES 38,000. MRI tax at 10%: KES 3,800 per month. Annual tax liability: KES 45,600. This host files a monthly return on iTax, pays KES 3,800 by the 20th of each following month, and declares the annual total in their end-of-year return. No other income tax applies to this rental income, provided annual rental earnings stay below KES 10 million.

Example 2: Two-Bedroom Apartment, Kilimani

Monthly bookings total: KES 95,000 (at approximately 72% occupancy). MRI tax at 10%: KES 9,500 per month. Annual tax liability: KES 114,000. This host is well within the MRI regime and should be filing monthly returns. Note that the KES 9,500 is owed regardless of whether the host had high maintenance costs or a repair bill that month — the MRI applies to gross receipts, not net income.

Example 3: Multiple Properties, Nairobi and Diani

Combined monthly rental income: KES 320,000 (KES 3,840,000 annually). MRI tax at 10%: KES 32,000 per month — KES 384,000 per year. Still within MRI territory since annual income is below KES 10 million. However, this host should also check whether they have crossed the VAT registration threshold of KES 5 million annually — if so, VAT obligations apply in addition to MRI tax. We cover this in Section 5 below.

The single most expensive tax mistake Kenyan hosts make is treating the 10% MRI as optional until they get caught. The penalty for unpaid MRI tax is 5% of the tax due plus 1% interest per month on the outstanding balance. A host who has been non-compliant for two years on KES 9,500 per month may face back taxes of KES 228,000 plus penalties that can exceed KES 50,000. Regularising early costs a fraction of this.

Filing Your Short Term Rental Tax Return in Kenya: Step by Step

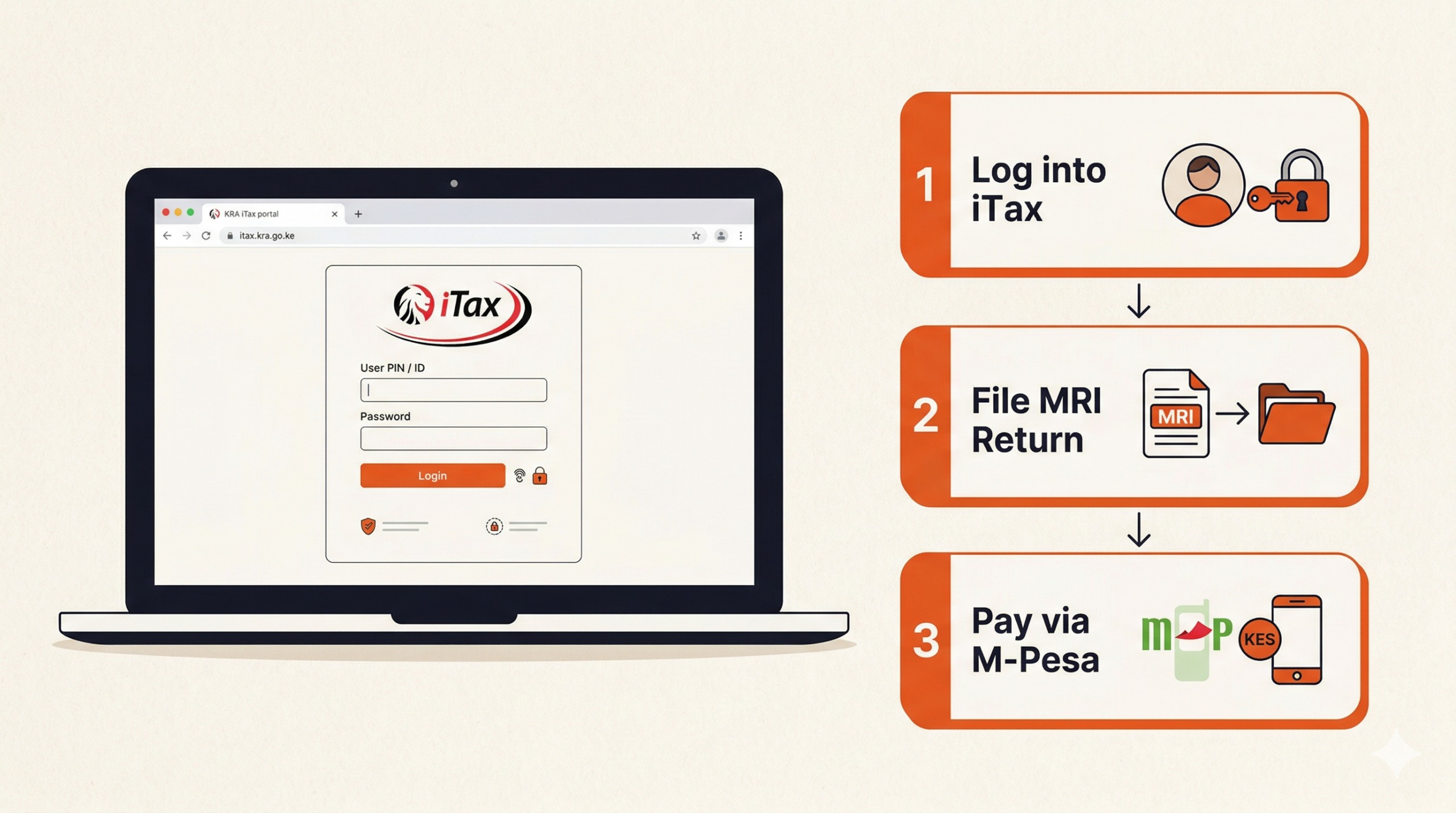

Filing your short term rental tax return in Kenya is simpler than most hosts expect. The process happens entirely online through KRA’s iTax portal, and once you have done it once, subsequent months take under ten minutes. Here is the complete process.

01

Get Your KRA PIN

If you do not already have one, register at itax.kra.go.ke. You will need your national ID, personal details, and a valid email address. PIN registration is free and takes one business day.

02

Log in to iTax

Go to itax.kra.go.ke and log in with your PIN and password. If it is your first time, you will need to reset your password using the temporary one sent to your email during PIN registration.

03

Select MRI Return

Navigate to Returns → File Returns → Monthly Rental Income (MRI). Select the month you are filing for. You will be prompted to enter your gross rental income for that month.

04

Enter Gross Income

Enter the total amount received from all short-term rental bookings during the month — the full guest payment, before deducting any expenses. The system calculates the 10% tax automatically.

05

Submit & Generate Slip

Review and submit the return. Download or note the payment registration number. You will use this to make the payment in the next step.

06

Pay via M-Pesa or Bank

Pay using M-Pesa Paybill 222222 (KRA), account number = your KRA PIN + tax period (e.g. PIN0102024). Alternatively, pay via bank or KRA agency. Deadline: 20th of the following month.

📅 Filing Deadlines

The MRI return for January must be filed and paid by 20th February. February by 20th March. And so on, every month. If the 20th falls on a weekend or public holiday, the deadline moves to the next business day. Missing a deadline triggers an automatic penalty of KES 1,000 per late return or 5% of tax due, whichever is higher.

VAT, Digital Service Tax, and Other Obligations

Beyond the MRI tax, some Kenyan short-stay hosts face additional obligations depending on their total annual turnover and how their bookings are generated. These are not edge cases — they affect a meaningful number of active hosts in Nairobi’s prime markets.

VAT Registration Threshold

If your total taxable turnover — from all sources, not just rental income — exceeds KES 5,000,000 in any 12-month period, you are required to register for VAT with KRA. Short-term accommodation is a VAT-applicable service in Kenya, and once registered, you must charge 16% VAT on each booking and remit it monthly to KRA. If you are approaching the KES 5 million threshold, speak to a tax advisor before crossing it — there are legitimate structuring options available to registered hosts.

Digital Service Tax (DST)

Kenya introduced a 1.5% Digital Service Tax on the gross transaction value of digital platform services. For platforms like Airbnb operating in Kenya, DST is collected and remitted by the platform itself on behalf of the transaction. However, if you are operating your own direct booking website — which Trubay Stayz hosts who take direct bookings through the platform may do — the DST question is worth clarifying with KRA or a registered tax agent to confirm whether platform-level remittance covers your obligation.

Annual Income Tax Return

Even under the MRI regime, you are still required to file an annual income tax return declaring all your income sources. Your monthly MRI payments are credited as advance tax against your annual return. This means that if MRI is your only income source, your annual return is largely administrative — the tax is already paid. However, failure to file the annual return is a separate violation that carries its own penalty.

Want to know how to maximise what you keep after tax? Our article on short-term rental income in Kenya shows you exactly what Trubay Stayz hosts earn — net, after all obligations are factored in. Read the Earnings Guide →

Penalties for Non-Compliance — and How to Avoid Them

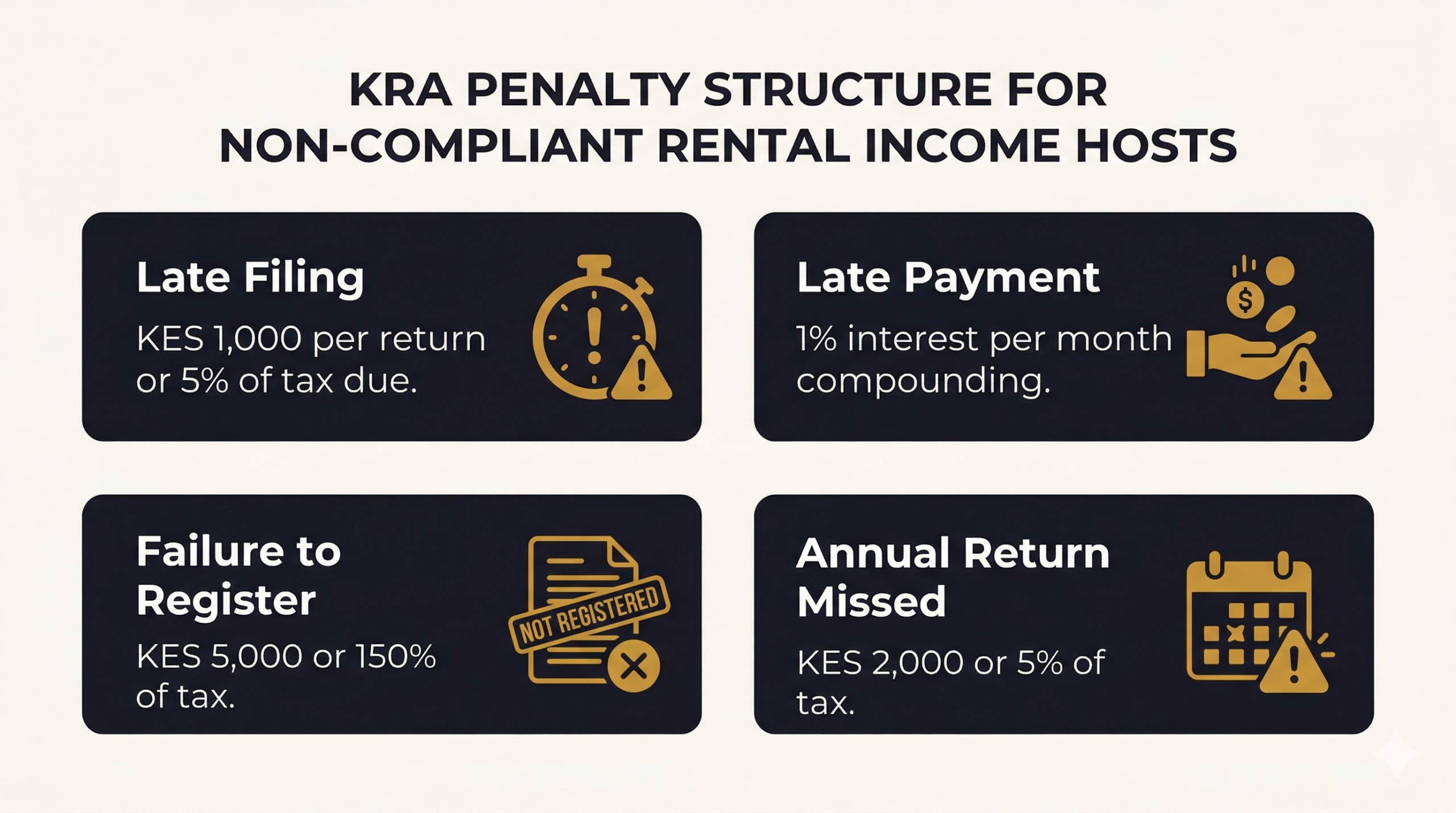

The KRA penalty structure for rental income non-compliance is specific and cumulative. Understanding it is not about fear — it is about making an informed calculation. Here is exactly what non-compliant hosts face.

- Late filing penalty: KES 1,000 per return not filed on time, or 5% of the tax due — whichever amount is higher.

- Late payment interest: 1% of the outstanding tax amount per month, compounding monthly until the balance is cleared.

- Failure to register: KES 5,000 or 150% of the tax that would have been due — a significant penalty for hosts who never registered at all.

- Failure to file annual return: Separate penalty distinct from MRI late-filing penalties. KES 2,000 or 5% of tax, whichever is higher.

- Deliberate tax evasion: In serious cases — multiple years of concealment, large amounts, or falsified records — KRA can pursue criminal prosecution under the Tax Procedures Act.

The practical path to avoiding all of these is straightforward: register your PIN if you have not already, file your first MRI return for the current month by the 20th of next month, and continue monthly from there. If you have historical arrears, approach KRA through the voluntary disclosure mechanism before they initiate an audit — the terms are considerably more favourable that way. For more on the complete legal framework Kenyan hosts operate within, our Kenya short-term rental laws guide covers the full regulatory picture beyond taxation.

What Changes If You Host Through a Registered Company

Some Kenyan property investors choose to operate their short-term rental portfolio through a registered limited liability company rather than as individuals. This changes the tax picture significantly. A company is not eligible for the MRI tax regime — it is subject to corporate income tax at a rate of 30% on net profits (after allowable deductions). For hosts with higher operating costs relative to income, the ability to deduct expenses under corporate tax can make the company structure more tax-efficient than individual MRI at scale. However, this calculation depends heavily on your specific income levels, cost structure, and whether you are also drawing a salary from the company.

If your rental portfolio earns above KES 5–6 million annually, the decision between individual MRI and corporate structure is worth a session with a registered tax consultant or accountant. The difference in annual tax liability can be substantial, and the compliance requirements under each regime differ significantly. For most hosts with one or two properties earning below KES 5 million per year, individual MRI remains the simpler and often lower-cost option.

Ready to list your property on a Kenyan platform designed around local compliance, M-Pesa payouts, and real host support? Your first listing takes under 30 minutes. List on Trubay Stayz →

You Know the Rules. Now Put Your Property to Work.

Join Kenyan hosts earning consistent, compliant short-term rental income on Trubay Stayz — with M-Pesa payouts and a team based right here in Nairobi. Become a Host on Trubay Stayz →

The short term rental tax rate in Kenya under the KRA Monthly Rental Income (MRI) regime is a flat 10% on gross rental income. This applies to hosts and landlords earning between KES 144,001 and KES 10,000,000 per year. Hosts earning below KES 144,000 annually (KES 12,000 per month) are currently exempt from MRI tax. Hosts earning above KES 10 million per year are taxed under standard personal income tax rates.

Yes. All rental income earned in Kenya — including income from Airbnb, Trubay Stayz, and direct bookings — is subject to KRA’s Monthly Rental Income tax if your annual earnings exceed KES 144,000. KRA has been working with digital platforms to access transaction data, and undeclared rental income is increasingly detectable. Declaring and paying your MRI tax monthly is far less costly than the penalties for non-compliance.

Rental income tax in Kenya is paid through KRA’s iTax portal at itax.kra.go.ke. You file a Monthly Rental Income return for each month by the 20th of the following month, and pay via M-Pesa Paybill 222222 using your KRA PIN as the account number, or via bank transfer. You will need a KRA PIN to register and file — PIN registration is free and available online.

Penalties for failing to pay rental income tax in Kenya include: a late filing penalty of KES 1,000 per return or 5% of tax due (whichever is higher), 1% monthly interest on any outstanding unpaid tax, and a failure-to-register penalty of KES 5,000 or 150% of the tax that should have been paid. These penalties compound monthly, making early compliance significantly cheaper than delayed action.

VAT applies to short-term rental income in Kenya if your total annual turnover exceeds KES 5,000,000 from all sources. Short-term accommodation is classified as a VAT-applicable service. Once you cross the KES 5 million threshold, you must register for VAT, charge 16% on bookings, and file monthly VAT returns with KRA. Hosts below this threshold are not required to register for VAT.

Under the Monthly Rental Income (MRI) tax regime, no expense deductions are allowed. The 10% tax applies to your total gross rental receipts regardless of maintenance costs, mortgage payments, furniture expenses, or platform fees. Expense deductions are only available to hosts who exceed the KES 10 million annual threshold and are taxed under the standard income tax regime instead.